A Fragile Consumer Economy Beneath Strong Headline Growth

On paper, the U.S. economy looks resilient. Unemployment remains below 4%, GDP growth is steady, and consumer spending continues to fuel expansion.

Yet beneath these strong macro indicators, household finances are weakening — fast.

According to the Federal Reserve Bank of New York, U.S. credit card debt crossed $1.2 trillion in 2025 — a record high. Delinquencies are rising, interest rates remain elevated, and more Americans are revolving balances month to month.

Economists call this a “silent leverage crisis” — not a dramatic collapse like 2008, but a slow, corrosive squeeze on household liquidity.

Anatomy of the U.S. Credit Card Debt Crisis

The U.S. credit card debt crisis stems from three intersecting pressures: persistently high borrowing costs, declining real wages, and inflation-driven dependency on revolving credit.

a) Interest Rates at Record Highs

The Federal Reserve’s tightening cycle pushed benchmark rates to 5.25–5.50%, the highest in over two decades.

Credit card APRs — which track the Fed funds rate — have surged to an average of 22.1%, according to the Fed’s G.19 Consumer Credit Report.

That means a household carrying a $10,000 balance is paying $2,200 per year in interest — even without spending another dollar.

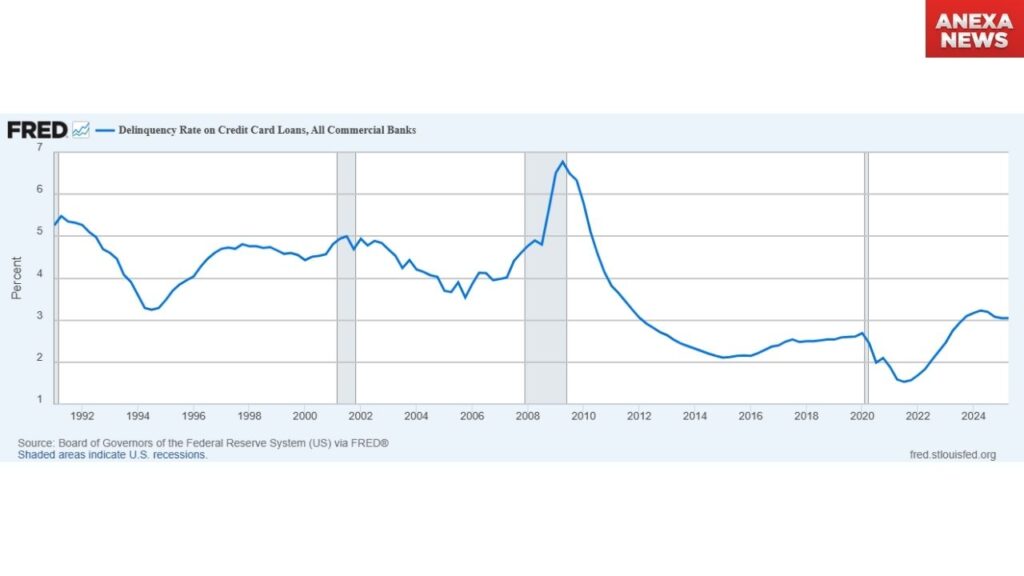

b) Rising Delinquencies and Utilization

Data show a clear trend reversal.

- 30-day delinquencies rose to 14.1% in early 2025 — the highest since 2011.

- Serious delinquencies (90+ days) reached 10.7%.

- Average credit utilization climbed to 29%, signaling that consumers are using credit for essentials, not luxuries.

Credit Card Delinquencies by Income Bracket, NY Fed 2025

The chart shows lower-income households (bottom 40%) now account for over half of new delinquencies, confirming that financial stress is concentrated among wage earners most affected by inflation.

c) Erosion of Household Liquidity

Even as nominal wages increase, real wage growth (after inflation) has stalled. Many households are now borrowing to maintain purchasing power.

The personal savings rate has dropped below 4%, its lowest since before the pandemic.

This toxic combination — depleted savings, higher interest costs, and growing delinquencies — forms the structural base of the U.S. credit card debt crisis.

Also Read: Will U.S. Mortgage Rates Drop in 2025?

Digital Behavior as an Early Economic Indicator

Beyond official statistics, online finance communities offer an early signal of consumer sentiment.

Analysis of Reddit’s r/personalfinance and r/povertyfinance threads in 2025 shows a sharp thematic shift — from wealth-building and rewards optimization to survival-oriented budgeting and minimum payment planning.

This qualitative sentiment matches the Federal Reserve’s Consumer Expectations Survey, which found that 46% of Americans now rank “debt repayment” as their top financial priority — up from 29% two years ago.

In other words, the stress visible in digital discussions is an authentic social indicator of financial tightening across income groups.

The Federal Reserve’s Policy Trap

The Fed faces a challenging policy dilemma in 2025 — balancing disinflation with household solvency.

a) The Lag Effect of Tightening

While inflation cooled to 3.1%, the aftershocks of higher rates are still working through consumer credit markets. Credit card APRs adjust almost instantly to Fed moves, meaning borrowers feel pain far sooner than mortgage or auto loan holders.

b) Why Rate Cuts May Offer Limited Relief

Even if the Fed begins rate cuts by late 2025, credit card interest rates are “sticky downward.” Lenders rarely reduce APRs proportionally due to higher default risks and capital requirements.

Thus, households may stay locked in high-cost credit cycles long after policy easing starts.

c) Macro Implication

Persistent revolving debt effectively tightens financial conditions from the bottom up — a self-reinforcing squeeze on disposable income that could restrain GDP growth through 2026.

The Structural Shift in Credit Usage

Traditionally, credit card balances tracked consumption cycles. Today, they track income shortfalls.

For millions, credit is no longer a convenience — it’s a core income supplement.

Data from the Bureau of Economic Analysis (BEA) show that credit-financed consumption now accounts for nearly 9% of monthly retail spending, up from 6% pre-pandemic.

That shift signals a deeper structural problem: credit dependency as a means of economic survival.

Comparison: Today’s Debt Cycle vs. the 2008 Crisis

While the credit card debt crisis lacks 2008’s systemic contagion, its distributed distress across households poses long-term economic risks.

| Factor | 2008 Housing Crisis | 2025 Credit Card Cycle |

| Primary Asset | Mortgages | Revolving Credit |

| Trigger | Leverage & Collateral Collapse | Income Compression & Inflation |

| Default Speed | Slow (6–12 months) | Fast (90–120 days) |

| Policy Leverage | Quantitative Easing | Monetary Easing with Consumer Lag |

Economists estimate that every 1% rise in credit card delinquencies reduces consumer spending by 0.2% in the following quarter.

At current trajectories, the U.S. could face a modest consumption slowdown by late 2025 — even without a formal recession.

Expert Answers

Q1: What’s driving the U.S. credit card debt crisis in 2025?

High inflation, stagnant wages, and 22%+ interest rates are combining to create unsustainable repayment burdens.

Q2: Is this crisis comparable to 2008?

No — 2008 was a systemic collapse; 2025 is a distributed liquidity erosion affecting millions of households.

Q3: Will Fed rate cuts solve the problem?

Not immediately. Credit APRs are slow to fall, meaning debt stress will persist into 2026.

Q4: How can households manage debt risk?

Experts recommend aggressive repayment on highest-APR cards, balance transfers to lower-cost options, and keeping utilization below 30%.

Forward-Looking Insight: Expert Forecast

According to Moody’s Analytics (October 2025 Economic Outlook), credit card delinquency rates are projected to peak at 11.5% by Q1 2026 before stabilizing as inflation cools and real wage growth resumes.

However, the report warns that “if energy or housing inflation resurges, the recovery in consumer liquidity could be delayed by another fiscal year.”

In other words, the path forward hinges on the Fed’s ability to engineer a soft landing without exhausting household credit capacity.

Also Read: Best Credit Cards in USA for Students

Policy and Market Implications

a) For Lenders

Banks face a profitability paradox: high net interest margins offset by rising charge-offs. Some regional lenders are tightening underwriting standards and reassessing unsecured credit exposure.

b) For Policymakers

Expect renewed focus on household financial stability programs — including expanded credit counseling access, enhanced disclosure rules, and incentives for low-interest consolidation loans.

c) For Markets

Investors should monitor credit-sensitive equities — regional banks, fintech lenders, and consumer retail — as rising delinquencies often precede margin compression.

Outlook: A Year of Balancing Acts

Heading into 2026, three variables will determine whether the U.S. credit card debt crisis deepens or plateaus:

- Inflation Trajectory — A faster disinflation path could ease pressure.

- Labor Market Stability — A rise in unemployment would accelerate defaults.

- Policy Timing — The Fed’s ability to pivot before household liquidity collapses.

Baseline forecasts suggest gradual stabilization by mid-2026, but the near-term outlook remains tense.

The Real Crisis Is Liquidity, Not Leverage

The U.S. credit card debt crisis is less about reckless spending and more about financial endurance. American households are absorbing inflation’s aftershocks through higher-interest debt, lower savings, and deferred goals.