The 2025 Federal Reserve rate cuts have triggered one of the most important financial shifts for U.S. households and investors. Whether you manage debt, own a home, run a business, or invest in the stock market, Fed policy is reshaping your financial landscape. Understanding how rate cuts work and what they mean for the economy helps you make smarter, faster money decisions.

What Is a Fed Rate Cut?

A Federal Reserve rate cut occurs when the Federal Reserve lowers the federal funds rate, the short-term interest rate banks charge each other for overnight loans. Although this rate is not directly used by consumers, it influences:

- Mortgage rates

- Credit card APRs

- Auto loans

- Personal loans

- Savings account yields

- Business borrowing

- Treasury yields

- Stock and bond markets

In simple terms: When the Federal Reserve rates, borrowing becomes cheaper—and saving earns less.

Key Facts About the 2025 Rate Cut Cycle

| Impact Area | Effect of Fed Rate Cut | Timeline Consumers Feel It |

| Mortgage Rates | Tend to decline, but lag the Fed | 4–8 weeks |

| Credit Card APRs | Fall as prime rate drops | 1–2 billing cycles |

| Auto/Personal Loans | Slight decline | 2–6 weeks |

| Bond Yields | Typically fall | Immediate |

| Stock Market | Often rises after first cut | Days to months |

| Savings APYs | Drop gradually | 30–90 days |

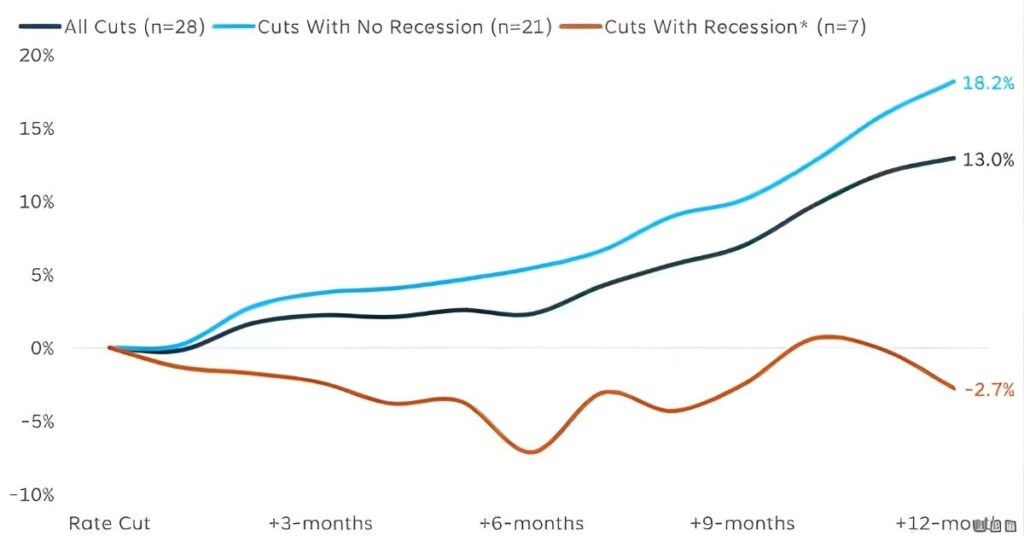

Chart 1: S&P 500 Performance After Historical Rate Cuts

This chart shows how the S&P 500 generally rises in the months following initial Fed rate cuts—assuming the economy is not entering a deep recession.

Key takeaway: Rate cuts tend to boost equities because borrowing costs fall and earnings expectations improve.

Why the Fed Cuts Rates

The Federal Reserve cuts rates when it sees:

- Slowing economic growth

- Declining inflation

- Rising unemployment

- Soft consumer spending

- Tight credit conditions

Rate cuts are intended to stimulate borrowing, investment, and job creation.

Also Read: How to Make Smart Money Moves After the First Fed Rate Cut of 2025

How Fed Rate Cuts Affect Your Money Immediately

1. Credit Card APRs

Credit card rates are tied to the prime rate, which moves with the Fed.

After a rate cut, APRs typically drop 0.25%–0.50% within 30–60 days.

This helps Americans carrying revolving balances—but interest remains high.

2. Auto Loans and Personal Loans

Rate cuts generally lower auto and personal loan rates slightly, usually:

- 0.20%–0.60% decline, depending on lender conditions

- Faster approval and refinancing opportunities

Consumers with 700+ credit scores benefit most.

3. Mortgage Rates

Mortgage rates respond indirectly.

They tend to fall over several weeks, not immediately, because they track Treasury yields and investor expectations. As inflation cools, lenders lower rates.

This creates opportunities for:

- Refinancing

- First-time homebuyers

- Investors using HELOCs

Also Read: How the Fed Rate Cut 2025 Affect Mortgage Rates and Home Buyers

4. Savings Accounts and CDs

High-yield banks reduce APYs 30–90 days after the Fed moves.

If you want to lock in higher interest, 1–2-year CDs are usually best before additional cuts.

Also Read: How the Fed Rate Cut 2025 Impacts Savings Account Interest Rates

Market Reaction: How Investors Should Think About Rate Cuts

Fed rate cuts create varying effects across asset classes. Here’s how markets typically react:

Stocks: Rate Cuts Usually Boost Performance

Historically, after the first Fed rate cut:

| Time After Cut | Avg. S&P 500 Return |

| 1 month | +1% to +2% |

| 3 months | +3% to +5% |

| 6 months | +5% to +8% |

| 12 months | +8% to +13% |

Sectors that tend to outperform:

- Tech

- Consumer discretionary

- Utilities

- Real estate (REITs)

- Industrials

Why? Because cheaper borrowing drives corporate investment and consumer spending.

Bonds: Prices Rise as Yields Fall

Lower rates increase the price of previously issued bonds.

Winners in a rate-cut environment:

- Long-duration Treasuries

- Investment-grade corporate bonds

- Muni bonds

- Bond ETFs (TLT, AGG)

Also Read: How Interest Rates Shape U.S. Stock and Bond Markets

Banks and Financial Institutions

Banks face pressure because:

- Net interest margins shrink

- Savings yields fall faster than lending rates

However, loan demand increases, balancing out some losses.

How Consumers Should Position Themselves in a Rate-Cut Cycle

1. Refinance High-Interest Debt

Rate cuts reduce financing costs. Consider refinancing:

- Credit card balances → into lower-rate personal loans

- Auto loans

- Student loans (private sector only)

- Mortgages (when rates fall further)

2. Shift Savings Strategy

To keep earning:

- Lock CDs before further cuts

- Use high-yield savings while rates still hold

- Consider Treasury bills during easing cycles

3. Adjust Investment Strategy

Financial analysts commonly suggest:

- Increasing exposure to large-cap U.S. equities

- Adding technology and utilities

- Allocating to long-duration bonds

- Limiting cash drag in low-yield accounts

Expert Insight

According to Moody’s Analytics, rate cuts stimulate borrowing and investment but can raise inflation risks if introduced too early.

According to Bank of America Global Research, U.S. equities tend to perform well during the first 6 months of easing cycles.

FAQ: How Fed Rate Cuts Affect Your Money, Loans & Investments

1. What exactly is a Federal Reserve rate cut?

A Federal Reserve rate cut means the Federal Reserve lowers the federal funds rate, which is the short-term interest rate banks use to lend money to each other. This decision influences nearly every U.S. borrowing and saving product, including mortgages, credit cards, auto loans, personal loans, and savings accounts.

2. How quickly do mortgage rates drop after a Federal Reserve rate cut?

Mortgage rates do NOT fall immediately because they follow the 10-year Treasury yield, not the Fed funds rate directly.

Historically, mortgage rates begin to ease within 4–8 weeks, depending on inflation trends and bond-market expectations.

3. Do credit card interest rates fall when the Fed cuts rates?

Yes—credit card APRs move based on the prime rate, which is tied to the Fed’s rate.

Most card issuers adjust APR within 1–2 billing cycles (30–60 days) after a rate cut.

4. How do Fed rate cuts affect the stock market?

Rate cuts typically support stock performance because:

- Borrowing becomes cheaper for businesses

- Earnings outlook improves

- Investors rotate money from bonds into equities

Historically, the S&P 500 rises an average of 5%–8% within six months after the first rate cut unless the country is entering a recession.

5. Do savings account and CD rates go down after a rate cut?

Yes. Banks usually lower APYs 30–90 days after the Fed moves.

High-yield savings accounts and CDs are the first to adjust downward.

6. Are Fed rate cuts good or bad for the economy?

Rate cuts can be good when the goal is:

- Preventing a recession

- Stimulating business investment

- Lowering debt costs for households

But cuts can be bad if:

- Inflation is still elevated

- Consumers take on too much debt

- Asset bubbles form

7. How do rate cuts impact bond yields?

Bond yields typically fall during rate-cut cycles.

As yields drop, bond prices rise, benefiting existing bondholders.

8. Should I refinance my mortgage after a rate cut?

Refinancing may be smart if:

- Your current rate is 1% or more above today’s market rate

- Your credit score has improved

- You plan to stay in the home long enough to offset closing costs

9. Do auto and personal loan rates fall when the Fed cuts rates?

Yes. Auto and personal loans usually decline 0.20%–0.60% within weeks after cuts.

However, the magnitude depends on lender competition and borrower credit risk.

10. When will consumers feel the full effect of a Federal Reserve rate cut?

Most households feel the impact within:

- 30 days → credit cards

- 30–60 days → personal loans

- 60–90 days → mortgage rates, HELOCs

- 90+ days → savings yields and CDs

11. Do Fed rate cuts cause inflation to rise?

They can. Rate cuts typically increase borrowing, spending, and hiring, which may push prices upward especially if inflation is already elevated.

12. What signals does the Fed look at before cutting rates?

The Federal Reserve tracks:

- CPI inflation

- Unemployment rate

- Wage growth

- GDP growth

- Financial market stress

- Global economic risks

Cuts are more likely when the Fed sees slowing economic growth and cooling inflation.

13. Are rate cuts guaranteed to boost the stock market?

No. If cuts occur during a recession, stocks may initially fall before recovering.

Market reaction depends on whether investors view the cuts as supportive or as a sign of economic weakness.

14. Should investors change their strategy during a rate-cut cycle?

Investment experts typically recommend:

- Increasing exposure to large-cap stocks

- Favoring technology, utilities, and real estate

- Adding long-duration bonds to benefit from falling yields

But the right strategy depends on your risk tolerance and time horizon.

15. How many times does the Fed cut rates in a typical cycle?

Historically, the Fed cuts rates 2–5 times during easing cycles, depending on economic conditions.

Final Thoughts

The 2025 Federal Reserve rate cuts are reshaping every aspect of the U.S. financial system—from mortgages to stock portfolios. Understanding how these changes flow through the economy helps you make smarter, faster, and more profitable decisions.

Whether you’re refinancing debt, adjusting savings strategies, or repositioning your portfolio, staying informed is the key to maximizing opportunities during rate-cut cycles.